The year 2021 was thrilling in so many ways. Everything went up, up, up (until it didn't). It was the best year financially so far in my whole life. Now, 2022 has been totally different and mostly wiped out already the gains I got in the previous year, but let's not focus on that right now. I'll make this a positive post about 2021 and I'll sulk on inflation fears, stock market crashes and WW3 later, ok?

Key figures from 2021

- Gross income: 222,953 €

- Net income: 145,005 €

- Investment gains: 0 €

- Expenses: 36,952 €

- Budget exceeded by 1,502 € (4%)

- Savings: 108,053 €

- Savings rate: 75%

During 2021, at one point my wealth had grown by over 250,000 €. I'm sure I don't need to calculate this, but that is quarter of a million. In one year! It was crazy. Then the stock market plummeted and I "only" ended up 100k up, completely by savings, not appreciation. But that's alright. If every year was like that!

Income

Most of my income came in the form of salary, but sadly, a small part of it was inherited.

And for those of you wondering if blogging helped: not really. Blogging income was negligible. After server bills and the accountant, I made 900 € net from blogging.

Here's the current run-down of the P2P platforms, some of which I still have a stake in.

| Platform | Return | stake | |

|---|---|---|---|

| Mintos ⭐ | 12% | review | ✔ |

| Estateguru ⭐ | 10% | review | ✔ |

| Lainaaja | 10% | ✔ | |

| Swaper | 12% | review | ✔ |

| PeerBerry | 12% | review | |

| NEO Finance | 12% | review | |

| RoboCash ⭐ | 11% | review | ✔ |

| Crowdestor ⭐ | 10% | review | ✔ |

| Bondora | 7% | review | ✔ |

| October | 4% | review | ✔ |

| Trine | 7% | review | |

| Sun Exchange ⭐ | 5% | review | ✔ |

| Reinvest24 | 6% | ✔ |

Additionally the duplex we rent out has an internal return rate of 40% at this point, but it is heavily leveraged and we got it under market price.

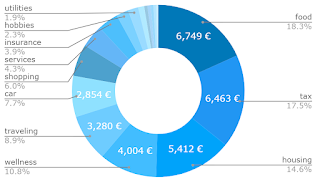

Expenses 36,952 €

🏛️ Extra income taxes 6,463 €

🏠 Housing 5,412 €

❤️ Wellness 4,004 €

✈️ Traveling 3,280 €

🚗 Car 2,854 €

🛍️ Shopping 2,002 €

🏦 Services 1,584 €

🛡️ Insurance 1,438 €

🎾 Hobbies 845 €

🔌 Utilities 714 €

❓ Misc 419 €

💳 Debt 227 €

🎞️ Leisure 219 €

✍️ Blogging 193 €

🚃 Transport 188 €

💰 Investing 143 €

The extra income taxes are annoying. I mostly count just net income, but having income increase so drastically, the tax authorities decided I should be paying extra income tax payments on top of what is withheld from my salary. I am going to try to change this for this year.

If I were to correct that, my expenses would be just 30,489 €. That's 2,541 € per month. With that expense level, my Number by the 4% rule would be 762,225 €.

Overall, my savings rate hit 75% in 2021 if I consider the extra income taxes as costs. If I adjust my net income and expenses with the extra income taxes, the savings rate goes to 78%.

I was trying to hit 80%, and could have if I had paid a little more attention.

Wealth

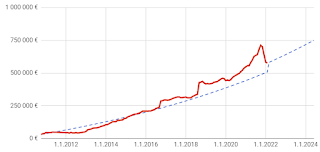

At the beginning of the year 2021, my wealth was at 537,808 €. By the end of it, it was 640,253 €. That's 84% from my Number.

Now, just brace yourself. I'm painting an overly positive picture and come 2022, this picture will change even more for the worse. But that's for later. I'll enjoy the sunshine for the duration of this post.

And now war

So I cannot help but to comment on the current world situation: the war in Ukraine. Us Finns have a very intimate history with Russia, losing a war to them in the WW2 and having the longest EU border with Russia nowadays. When a Russia starts a war that has such a major impact on global economy, there are two major motivations for me to comment.

The first thing to note is that there are no absolutes: Putin is out of his mind and could decide to do whatever. Saying they won't expand the aggression to other countries is equally unintelligent as saying they will. Only uncertainty is certain for now. Uncertainty usually opens up good opportunities economically.

My plan is to keep working and staying invested and diversified. This now feels like I will definitely miss my original target of hitting 1,000,000 by 40. The goal has moved at least two years forward. At the same time, the goal feels much less important now, after COVID and all, as other priorities have surpassed it, like enjoying life, investing on mental health, friends and family.

The war will impact everyday life for people and businesses, so risk has increased. What that means for peer lending for example is that you need to expect higher risk and therefore higher interest rates. Stock market has already largely reacted, so it's not obvious we will go much lower - but we might. I've been buying lately, even on credit.

As an working, accumulating investor with still years to retirement, you should welcome these situations where you get to buy cheaper, even if the world seems to spiral into chaos - or perhaps precisely because of that.

We who are fortunate, need to help

The impact in Ukraine is devastating, but helping is easy. While there are many options for you to help, the easiest I found was by donating e.g. just 50€ to the armed forces of Ukraine, which helps equip the army to fight back. It's a simple online form that takes a credit card.

If you'd rather donate in crypto currency like BTC, ETH or USDT, check this tweet instead. Don't make it a difficult decision, just donate. I have too.

No comments:

Post a Comment